Realized gain is actually not so fruitful exercise other than incidental situation to rebalance the portfolio or when there is fundamental change in the company. If one does not have the main mindset of continuing run the dividend business through compounding the portfolio growth with long term skin in the game, this strategy will be painful to your Health. haha. So the first mindset is, we don't realised capital gain or cut loss unless specific condition as mentioned is needed.

Quality Companies come with a price. Reits performance are usually ties to Sponsor, Credibility, Capability and Business. A good sponsor provides support of low funding cost when Reits borrows from the bank. The Reit/Sponsor Credibility is the most important however but as long it satisfies enough returns in a Win-Win situation, investors will be willing to push up prices. Management capability play a big part too. Another key area is the business type. I won't be interested in Ship Business as their depreciation is real and heavy whereas investment in properties are much more robust and can even grow with inflation.

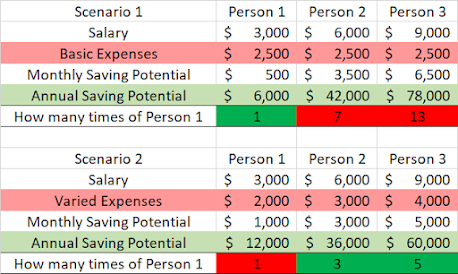

Yield is tricky. Forward yield is more relevant than current yield when comes to long term investment. It helps to support price and if it doesn't, an opportunity to average down for higher dividend returns in the future with lower cost. Current yield can spikes due to decrease in stock price. So one must do their home work to understand the mechanics on price decrease reasons. If a Reit is sold down without good justification, is a gem to get them. However if we are anticipating consistent poor performance or ticking time bomb ie. First Reit sustainability of contract, high yield can also be a Warning to avoid. When a yield keeps going lower but DPU maintains well, this likely due to increase in stock price. That's mean the Reits are probably doing it right and if this can last over a long time it will look more expensive. There could be situation where the DPU drops with increasing stock price. The Market may feel good about the future but one has to make sure stock price can be sustained.

Business Risk comes in many form. Short Lease, Depreciating Currency, Poor Future Contract, Poor Cycles, High Borrowing Cost, High depreciation, High maintenance cost, High Perpetual Cost, High Gearing, Bad acquisition/Sales, High Taxes, ... . If we feel a specific event could change the dynamics significantly, we may need to re-balance or cut loss. This has nothing to do with whether I still make money from the current investment or not.

Diversification to me helps to mitigate my wrong choice. ie. Retail Reits. For example I use to have CICT mainly. But today FCT is more but I still retain some CICT. In-addition I have MCT on accumulation path for months. Many decision needs not be 1 or 0. Of course to maximize profit, we may have to do that and this are probably for Experts. Am I ? It also depends one's risk appetite. Between counters I may do within sector rebalance as needed with changing market situation. There is also need to look at broader and deeper diversification such as Industrial Reits due to Covid.

This result a Portfolio of Reits where we can play around the allocation with specific needs. If we do this right, we will see compounding growth in Value and sustainable Dividend over many years. After learning for many years, maintaining a dozen stocks of Reits are not really hard because the business usually are not difficult to understand unless one try to be picky say between 1.1 or 1.2 performance differences. And I could be wrong and still be ok and will not be left far behind. Will there be a day we will see a large fall in our portfolio. You Bet ! A 1M size on large crash say 50% drop, is 500k capital loss. A big test on you. Will you Hold, Buy or Sell ?

Thinking ....

Cory

2021-0611

Articles in this Blog is personal take and educational purposes only. Reader should seek their own professional help when making financial decision and be responsible for their decision.