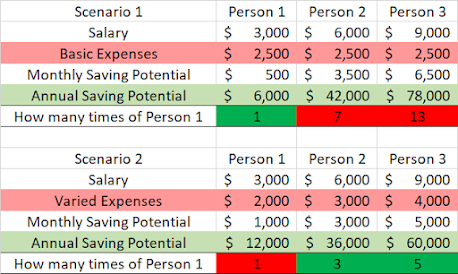

Not in any specific order, I am writing them down as notes as it comes off my mind for the past few days. No right or wrong but welcome to correct any errors.

1. Using CPF to pay for the housing

I think every couple should own their first property a HDB. Is the most affordable and one should only buy the right size that fits their income. If overstretch, relationship can be bad. And couple could be stressed. Happy family, happy life, and good health.

Question will be should we tap on CPF to purchase the property ? No right or wrong imo due to different circumstances. Just to be aware that there is accrued interests that we need to pay back to our own CPF account generally. Reason being I view CPF guaranteed returns are attractive and it makes sense for me to refund using idle money in the bank.

For my case, my SA account is not filled therefore VHR makes sense as I will do OA to SA transfer immediately after. So now hit FRS. After which I can do VC3AC to build up my SA further. There is annual limit of $37740 for MC+VC.

2. Condo Maintenance is sizeable

Let say $300 monthly. This is equal to $3600 annual ! And as I know this is generally paid by landlord if you rent out. So if one has no plan to use the condo for investment returns rather home stay, there is cost attached. In-addition there are gov benefits that ties to type of housing you live in. However life on earth is limited and each one has their own lifestyle. Make the full use of it.

3. Monthly Instalment there are 2 portions

Why I mention this is because the impact from interest rate is mitigated as time past due to large portion of our monthly installment is for paying down the principal loan. One reason why I refinance to a Fixed rate loan for 5 years. Lock lower rate on surface but also bought 5 years.

4. Property Tax

Yes, there is a cost. Period. In-addition I missed my 2nd payment because they switch to paperless without my explicit approval. They then allow me pay up without penalty for this time only. I feel like kenna kick and still have to bow to them. Life is Brutal next to Arrogant.

5. Employment/Income Risk

You will be tied down. Risk of unemployment. Age risk. At age 51, if I am out of job, what is the chance that I can find another similar paying job within one year ? And if I could not, maybe is unlikely 5 years down the road. To mitigate this, do you think 1 year emergency fund enough ? So chances are is either get another job quickly at much lower pay of mismatch skillset or plan to be retired regardless I like it or not. Yes, is a waste of my skill but bo pian.

6. Loan Year Restriction on Age

This is big for me because of my older age I can only borrow for 14 years max today. What this mean is my monthly amount will be much larger due to shorter loan period and need to meet the TDSR the same time. So if I plan to buy my next property, I will need to pay much more in cash.

7. Rental Income

For $3000 monthly rental, annual income is $36,000. This is good amount to offset loan payment for investment property at my age. Therefore I would only own more properties if regulation is more relaxed. There is risk if we do not have stable income or saving asset, we could panic. So we need to plan right as at current yield for my age, many properties are cash flow negative due to shorter loan period even though long run I will still be on top.

8. HDB or Private Property Loan

1% rate difference for $500k in simple term is $5k annually. Not cheap. So if I am to take HDB loan, make sure is worth it as it is much more expensive. I don't think it makes sense that people take HDB loan to minimize their chance of returning HDB flat if they failed to pay up. Either they overspend or cannot afford it in the first place.

9. Condo Space

Space is much smaller for New and Private. So if want to stay in one make sure we buy the size we want in number of rooms and total psf. If cannot afford, think twice. However if target rental, not sure 1 or 2 bed rooms are better. I do see quite a number of rent for 3 bedrooms just not as many. Due to gov curbs on number of properties, getting the larger affordable unit will be a better choice.

10. Home Ownership

Shifted homes from HDB 1 room, 3 room, 4 room, 5 room and Condo. Can be due to family size, estate renewal, working distance, upgrade, etc. home is not forever because is not my experience. We move and change with times and needs. However each time we move, is for better.

11. Invest in Property or Reit ?

I do both. I think maybe good to have at least one rental property income for diversification. Do be prepared for cash flow negative periods due to increasing price. Currently I use a chunk of the Reit dividends to top up the differences.

12. Location Matters

for OCR, Integrated central location, the psf is much higher than 5 min or 10 min away apartment. Delta can be more than 300 psf. However once top, the psf increase for good location increased by 30% with good rental value. So rental investment wise, a key consideration ?

13. Renovation Cost

As condo is half furnished, there is some saving. I do the fan, lighting and curtains. However due to limited space, customized bedding needed for smaller room. In total less than 15k i think.

14. Store room

Being used to store room in HDB, quite surprise the Condo unit I have do not have one. Many things are thrown before we move in. Minimalist by circumstances ?

15. Weather

Choose the NS direction. There are swimming pools below about 30m away to the side. So is not noisy.

As the unit is inward facing and unblocked, the temperature is quite cooling. However clothing takes longer to dry.

16. Leverage " Demon "

Property is high leverage considering for first property say we pay only 20%. So any gain or loss, magnifies. However there is cushioning from Rental income. Say over 5 year we make 250k for 1M apartment, the money put down including cost could be only 230k. So returns easily 15% annual for past 5 years excluding Rental Support. If we include say 30k annual rental income after cost, the returns will be roughly = 34% annual ! The range can be between 30% to 40% due to actual sell price 5 years later cannot be confirm .(updated)

I put item 16 the last because I want people to think hard about it.

Cory

2021-0413

Articles in this Blog is personal take and educational purposes only. Reader should seek their own professional help when making financial decision and be responsible for their decision.