Has been working on a new set of key parameters of determining how it is going to work out with my retirement planning adding in logic on cash flow into play. The goal is try to make it more realistic. However this means a lot more mathematics using Excel. To save some headache, not going to show the spreadsheet on how it is calculated but just the results and variables which will described here.

Inflation

The first thing to hit the wall is how much inflation figure to use when current inflation is sky high. A quick search into the internet seems to suggest 3% is a figure of reasonable value. Putting too high and you will find money never enough whereas putting too low might undermine your lifestyle in the midst of your retirement. That's how scary inflation can be when you try to incorporate inflation into your assets and probably explains why Fed is desperate to tame it even if this causes recession. In another perspective, once we hit 80s spending will be slower and this will help mitigate expense rate misjudgment.

Expense

From below table achieving $8220 will be nice. Currently Portfolio is at 5% yield due to some growth stock and Non-Reit lower yield counters. An All Reit portfolio probably can achieve 5.5% yield. A market correction may give the opportunity to push for 6% yield which at this point of time will need some major correction to arrive but provided there is cash reserve to invest.

Investment Returns

On the flipside of inflation is portfolio returns. Unless one has gigantic net worth, most people may have to depend on retirement program and investment returns to support a reasonable expected lifestyle.

Some would say their expense is low and this could be very well be the choice when option is limited. Another pitfall is if one is to consider investment equation, there is not much room to wait for market to rebound in a market correction which can last for many years. Dividend strategy could be the better key to enable planned retirement with greater certainty and there maybe decision to make on how much to allow for growth stocks on the point of retirement. So using dividend yield will be a good gauge for equity which can be around 5%. One could also use decade performance to move up the needle a little due to growth stock or capital gains. Say 8%. So a middle ground of 6.5%.

Other returns of different yield from equity such as SSB can do direct addition on capital returns. So are CPF returns.

|

| Click to see sharper picture |

How Lasting is the Portfolio

What is a divergence portfolio ? Meaning over time the portfolio is growing in retirement phase therefore above consumption needs. This is a goal.

When I first started, the plan is to have a divergence growth in the portfolio. That's not easy which I found later and will need sacrifices once I have to feed my home loan. It will be good to plan one's lifetime in decumulation phase. Is counter intuitive in eating into one portfolio that generates income but that is probably likely most people will have to for their retirement. Able to last till age 100 will be reasonable as chance are there are some sandbagging already.

Buffers

At this point of time, the buffer is Insurance policies, War Chest and Emergency Cash. Later retirement can be a good option too.

In-addition, Part Time Work for those who do not have choice. The retirement cashflow is greatly relieved for one who can find some part-time work for a few hours. Reason being likely it will scaled with inflation on top of CPF contribution into SA and OA, and will supplement overall return even if is a fraction of previous full-time employment work.

For those who has strong preference for Inheritance, either Property or Divergence Portfolio can do. If one can do both that means likely far ahead from the rest financially.

Returns consideration into the Cashflow

Assuming one retired and no other alternative of income.

1. Equity

2. CPF

3. SSB

4. Rental

5. Multipliers

Scenarios

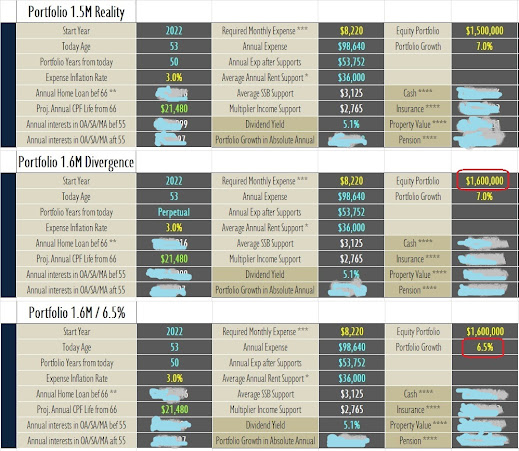

Scenario 1 simulated a lifestyle that requires 1.5M of 7% annual return to support $8220 expenses at 3% inflation rate. Portfolio able to last 50 years.

Scenario 2 bump up the portfolio to 1.6 M reaching divergence goal. Just $100k makes s a difference.

Scenario 3 pulls down the portfolio annual returns to 6.5% while maintaining 1.6M Portfolio size.

Portfolio able to last 50 years. Just 0.5% return difference.

There are many other variables depending on age, rental income, home loan size, CPF size etc. Many scenario one can do.

Cory

2022-0626

CoryLogics Invest Chat - No Coin, No Porn, No Penny

Articles in this Blog is personal take and sharing purposes only. Reader should seek their own professional help when making financial decision and be responsible for their decision.