Reflections on Parenthood and Financial Planning

When my first daughter was born, we were overjoyed. It was an extraordinary feeling to witness a living being emerge from the love my partner and I shared—something that transformed my life from solitude to family. We were busy, but our finances were manageable. There was still a fire in my belly when it came to work, especially since it was pre-COVID—specifically, the year 2019.

The Decision for a Second Child

We decided to have a second child, Rui. However, this journey was not as smooth sailing as the first. We faced medical complications both before and after her birth, leading to rising medical bills and increased stress in managing our finances. Fortunately, I had been investing in dividends for some time, which, along with our jobs, allowed us to manage our expenses exceeding $130,000 annually.

The Challenge of Time

The hardest challenge we faced was time. Money often became a means to buy time, which we realized was incredibly important. Soon enough, we noticed that Rui's development was lagging behind her peers by one or two years, despite the care she received. We recognized that she would likely need more attention and support before entering primary school.

I hinted to my boss about any potential retrenchment packages, but there was no budget allocated for such initiatives. Eventually, significant organizational changes at the management level created opportunities for layoffs funding this year. Thankfully, I am qualified and given Early Retirement instead, which comes with much larger compensation.

Early Retirement

Over the years, I have simulated various asset and portfolio scenarios to support this decision. I started with achievable lower goals and gradually increased them as I refined our strategy while working and watching our children grow. Despite my previous efforts to calculate the amount needed for retirement, I found that it was never quite enough mentally. One just has to bite the bullet and take it. The rationale is simply that my children are growing up and my age cannot wait. I do not want to miss their growing-up period too.

Now that Rui is four years old and with limited time on our hands, I conducted yet another rough financial analysis based on the proposed early retirement package. Interestingly, I may also qualify for additional pension benefits due to a long overseas assignment. While it’s not a substantial amount, it could help offset local taxes.

Financial Position

Today, I believe with confidence to be a point where I do not need to draw down from my portfolio assuming my expenses stay at the current level including inflation. Same time I've reduced risk levels in the stocks I've chosen and increased my fixed income investments as an emotional buffer. Managing my housing loan effectively has provided leverage without becoming a burden; I've calculated this based on cash flow principles.

A crucial aspect of our financial strategy is that my partner is still working and has her own savings. This gives additional peace of mind. While I cover most family expenses, she manages her basic needs and occasionally contributes financially. This arrangement works well because I want her to build her long-term insurance savings for added emergencies.

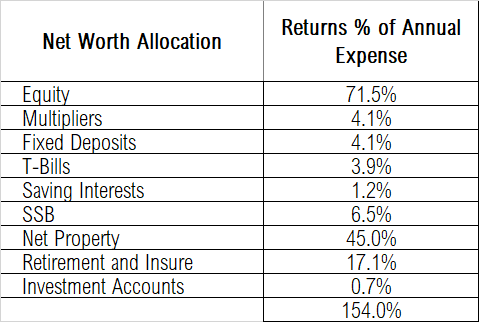

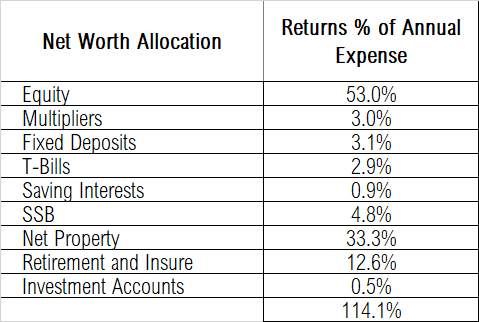

Financial goal calculation is a moving target to start with. For instance, I initially targeted an annual investment income of $48,000 in my early years and later pushed that goal up to $60,000 or more in stages. To expedite this timeline, I implemented a plan for drawing down from the portfolio while also maximizing contributions from CPF (Central Provident Fund), pensions, and fixed income investments.

Recent increases in rental income have also contributed positively. Although not all strategies were easily implemented or successful, starting early with saving and compounding made a significant difference. As we finetune the plan, we also make the bar higher when possible such as allowance for larger expenses or add inflation buffer. (

link on calculation )

Supporting Family

While it may be a taboo subject for some, I think it is important to share this as it can also be part of the critical equation when it comes to retirement. We do not hope to leave anyone behind. I have always contributed significantly to supporting my parents since my single days—a practice that continues today which I have refused to cut so far.

Fortunately, if necessary, I could reduce this support without significantly impacting their well-being; however, this would be a last resort as they are now advanced in age. There are not many years I am allowed to provide them.

Cory Diary

2024-11-16

CoryLogics Invest Chat - No Coin, No Porn, No Penny

Disclaimer: The articles presented in this blog reflect personal opinions and are intended for informational and sharing purposes only. Not responsible of errors. Readers are advised to seek professional guidance when making financial decisions and should take full responsibility for their choices.