Retirement is often viewed as the final chapter of one's career, and for many, the retirement package represents a significant financial milestone. This package can serve as a substantial boost to one's savings upon retirement, providing a sense of security and opportunity for investment. After careful consideration over several months, I have decided that my retirement funds will be allocated entirely into a War Chest—a strategic reserve for future investments.

Rationale Behind the War Chest

The primary reason for this decision is the current state of the market. We are already experiencing a bull market, which means that prices are generally rising. Entering this market with a large sum of cash could be illogical; instead, I believe it would be more prudent to wait for the next investment opportunity. Historically, markets operate in cycles, and while we are enjoying a bull phase now, it is inevitable that a downturn will follow. By holding off on immediate investments, I can position myself to take advantage of future opportunities when they arise.

In the meantime, I plan to distribute my funds into fixed-income instruments that prioritize capital preservation. Options such as Treasury bills (T-bills) are an excellent choice due to their low risk and government backing. T-bills provide a secure way to earn interest while ensuring that my principal investment remains intact. Additionally, other government-backed securities can offer similar safety and stability, making them ideal for retirees seeking to safeguard their capital.

Equity Portfolio Considerations

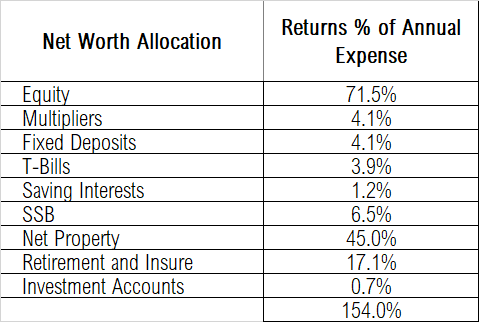

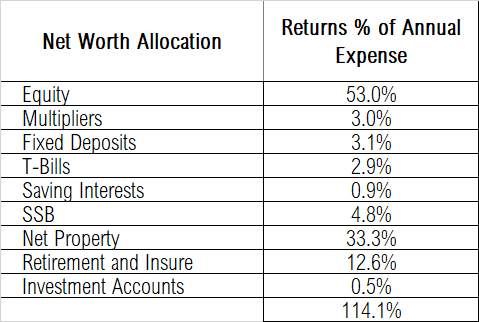

In addition to my War Chest strategy, I have allocated a significant portion of my net worth—approximately one-third—into equities. If the current bull market continues, this allocation could yield substantial returns. Investing in equities typically involves higher risk but also offers the potential for greater rewards compared to fixed-income investments. Therefore, maintaining a balanced approach between equities and fixed income is crucial for optimizing my retirement portfolio.

Managing Outstanding Loans

As an early retiree, I still have outstanding loans that need to be managed carefully. Having access to ready funding is essential in case of emergencies or unexpected expenses. This financial cushion allows me to navigate any potential challenges without compromising my long-term investment strategy or financial goals.

In conclusion, my retirement planning revolves around strategic decision-making focused on preserving capital while remaining poised for future investment opportunities. By establishing a War Chest and diversifying my portfolio across fixed-income instruments like T-bills and others, I aim to secure a stable financial future while being prepared for any challenges that may arise along the way.

Cory Diary

2024-12-16

CoryLogics Invest Chat - No Coin, No Porn, No Penny

Telegram CoryLogics <= Link to Telegram Chat

Telegram Cory Channel <= Link to Channel

Disclaimer: The articles presented in this blog reflect personal opinions and are intended for informational and sharing purposes only. Not responsible of errors. Readers are advised to seek professional guidance when making financial decisions and should take full responsibility for their choices.