Millionaire

In 2023, achieving millionaire status in Singapore after 20 years in the workforce is not an unattainable feat for those with reasonably good jobs and savings. The compounding effects of CPF and Property appreciation have made it easier to reach this milestone. However, missing out on either of these can have a significant impact on one's finances.

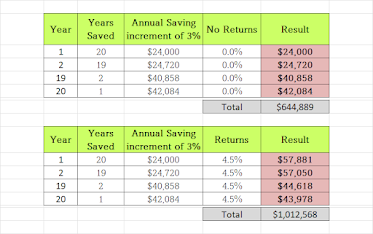

For those who have not yet reached millionaire net worth, this could be due to personal or family commitments. However, it is important to note that a million dollars today is not the same as 20 years ago. Assuming a typical job that allows for annual savings of $24k, a 3% annual increase with no investment or a 4.5% return on investment can make a significant difference over 20 years.

Below table tells you the differences in total after 20 years.

Managing Risks

Investing in something that provides a 4.5% return, such as CPF SA at 4%, is a good base as the capital is protected. Reits, stocks, properties, SSB, and FDs are also options, but it is crucial to ensure that the principal is not compromised and to understand the cost of capital if investing outside of CPF.

Recent research on millionaires shows that equity is not the primary path to wealth. Cash, bonds, property, and business also play a significant role. As a salaried worker, it may not be possible to have a business, so it is essential to allocate net worth across different categories. The chart below shows a typical allocation for net worth, but it is important to note that movement between categories over time is necessary to arrive at this point.

Overall, achieving millionaire net worth is achievable with discipline and smart investment choices. Building a diverse portfolio and allocating net worth appropriately can help achieve financial goals and provide peace of mind in the long run.

Net Worth Allocation

Below is chart that I am tracking into. As a typical salaried worker I do not have business. There is minimal buffers in my computation so no sandbagging. What we don't see is the movement overtime between the categories to arrive at this point. For example one could have sold a property and realised large amount of cash previously. So read it as current status on allocation.

Chart allocation of Net Worth

Broadly speaking, this looks quite similar to peace of mind plan. I would like higher value in property allocation and this take it's own time to materialize as in possible property appreciates while other categories reduces through expenses when we step into retirement mode.

Cory

2023-03-29

CoryLogics Invest Chat - No Coin, No Porn, No Penny ( Limited to Invitation )

Telegram CoryLogics <= Link to Telegram Chat

Articles in this Blog is personal take and sharing purposes only. Reader should seek their own professional help when making financial decision and be responsible for their decision.