Shifting Strategies

As we navigate through the intricate landscape of investment, it becomes imperative to reassess our equity portfolios, especially in the face of fluctuating market conditions. With the Federal Reserve hesitating to adjust rates as expected and a mix of thriving and sluggish markets, it's time to delve into the strategic adjustments made in recent weeks.

Dropping Google

Despite its dominant position, Google appears to be lagging in the rapidly evolving tech landscape. Questions arise about its adaptability and potential disruption. Personal experiences with Google's desktop functionalities and YouTube recommendations have been underwhelming, with concerns about malware hijacking further exacerbating the user experience. While Google still holds prominence, and I will be back quickly. Meantime, cash raised from the sale.

Adding UOB

Amidst the goal of mitigating portfolio volatility, a strategic move was made to incorporate UOB into the equity mix. With a sizable allocation already in DBS and OCBC, UOB's inclusion diversifies the bank exposure effectively. This decision brings the banks' allocation to 36.5% of the equity portfolio, offering a hedge against REITs exposure while supporting dividend strategies. Despite prevailing concerns, current pricing suggests banks are not overvalued, with recession risk looming as a key watchpoint.

Monitoring Distressed Stocks

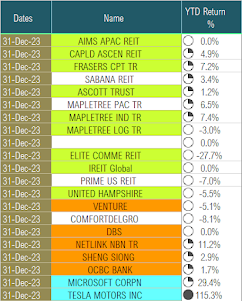

The portfolio hasn't been immune to challenges, with certain stocks facing continuous declines. Specifically, iReit and Elite Commercial Reits have experienced capital losses attributed to macroeconomic factors such as high interest rates and exchange rate fluctuations. However, their valuations remain comparatively stable against US Office REITs, prompting a decision to maintain positions, anticipating potential recovery as market conditions evolve. The fortunate thing is they have been sized-investment so their impact is not significant so far. Each year we can only afford a few small lemons so we need to constantly remind oursleves in our picks and allocation.

Conclusion

In the ever-changing investment landscape characterized by global market dynamics, proactive adjustments are essential to optimize portfolio performance and manage risk effectively. By scrutinizing each component and adapting strategies accordingly, portfolio can navigate uncertainties while positioning for long-term success. As we progress through 2024, vigilance and flexibility will remain paramount in capitalizing on emerging opportunities and mitigating potential setbacks.

Cory Diary

2024-03-22

CoryLogics Invest Chat - No Coin, No Porn, No Penny ( Limited to Invitation )

Telegram CoryLogics <= Link to Telegram Chat

Disclaimer: The articles presented in this blog reflect personal opinions and are intended for informational and sharing purposes only. Not responsible of errors. Readers are advised to seek professional guidance when making financial decisions and should take full responsibility for their choices.

{kind=link}